Algorithms.

Evolved.

Independent, research-driven

execution algorithms, trading technology, & trade analytics

Unconflicted algorithmic execution backed by empirical research

An end-to-end, global execution platform for equities and futures

The science behind every execution

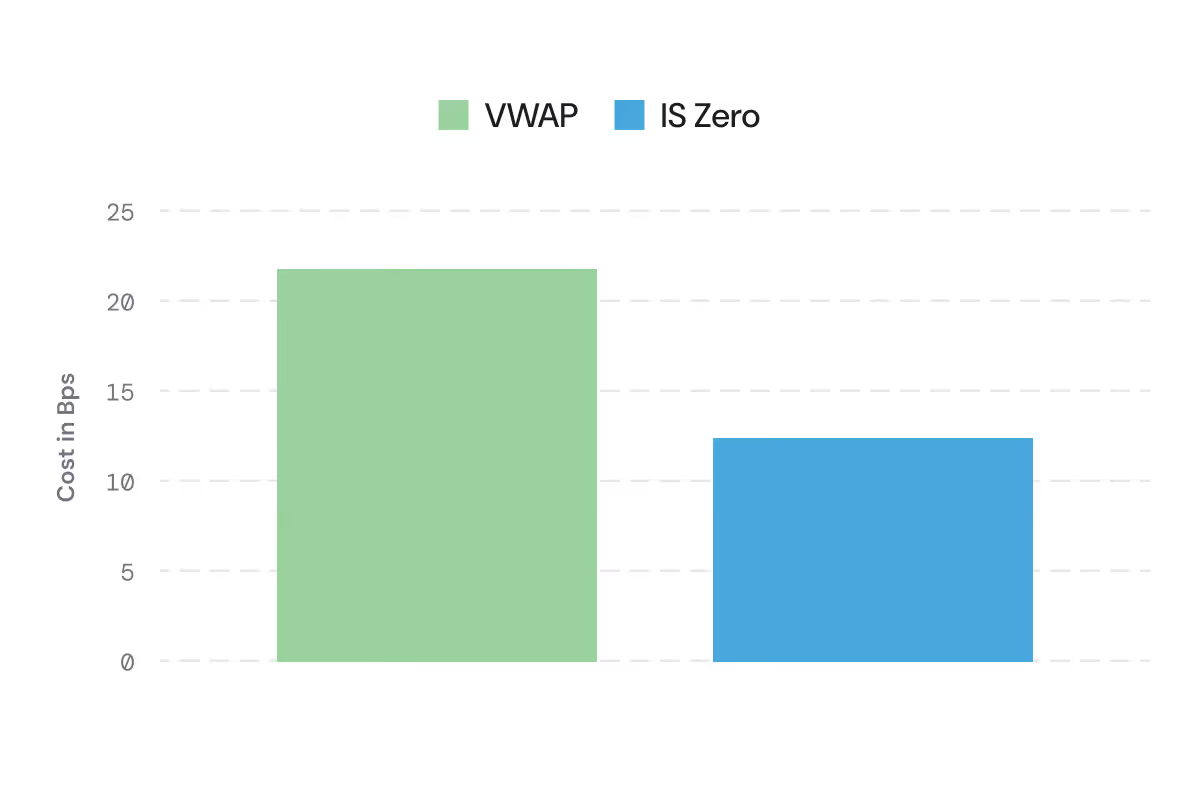

IS Zero: Reinventing VWAP algorithms to minimize implementation shortfall

Many traders use VWAP to minimize IS for low-urgency orders, but VWAP ignores intraday volatility. IS Zero integrates both volume and volatility expectations, reducing IS slippage over VWAP by 37% in equities A/B testing across tens of thousands of parent orders.

37%

cost reduction vs. arrival

In a sample of 140,000 sample orders, IS Zero reduced arrival slippage by 37% over the VWAP algorithm.

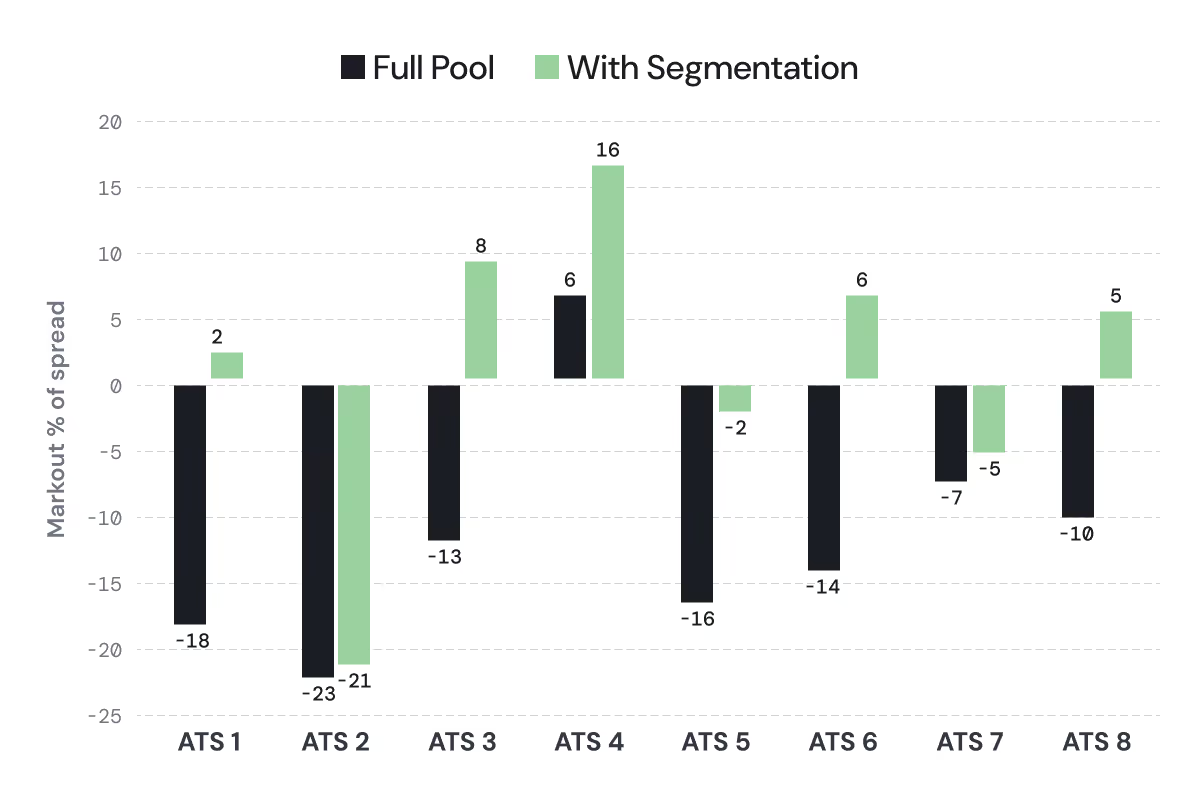

The Playbook for Curating Liquidity in US Equity ATSs

Most execution algorithms can access most ATSs but connecting to a venue is not the same as knowing how to use it. This paper presents the framework behind Curator, our dark liquidity aggregation algorithm, covering ATS segmentation, tactic selection, proprietary signals, conditional orders and a practical playbook for measuring and adapting as conditions change.

Venue segmentation is effective but the magnitude varies. The chart above illustrates comparison of Full Pool to Tier 1 (highest quality) at corresponding pool.

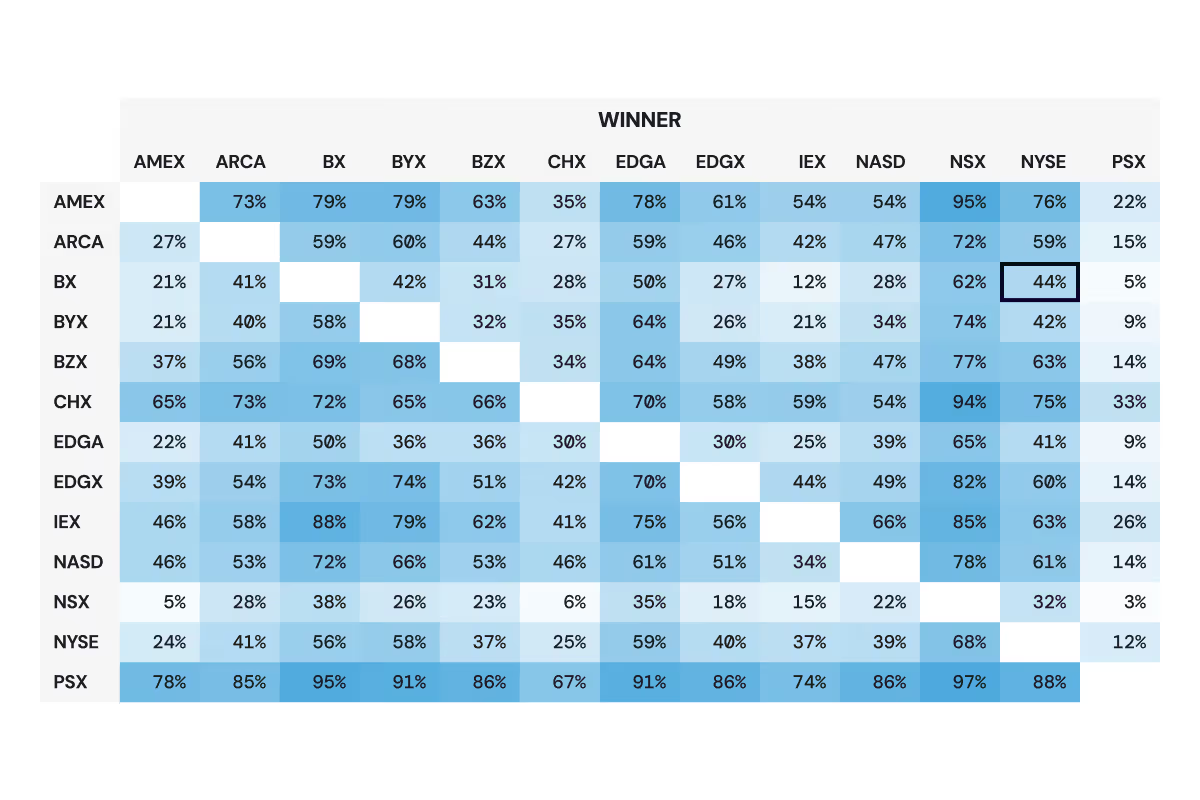

Queue-Jumping & Strategic Limit Order Routing

With 16 exchanges competing for each order, choosing where to post limit orders is a complex problem. Static venue selection leads to significant performance degradation as orders get "queue-jumped" by participants posting on higher-priority exchanges. We present a WinMatrix that helps identify which exchange will receive the next marketable order given 65,535 possible combinations of competing exchanges.

0.65 bps

IS savings at parent order level

The WinMatrix summarizes exchange competitiveness. The black box highlighted above indicates that for this stock, NYSE receives a market order 44% of the time when it and NASDAQ BX are competing (BX is inverted).

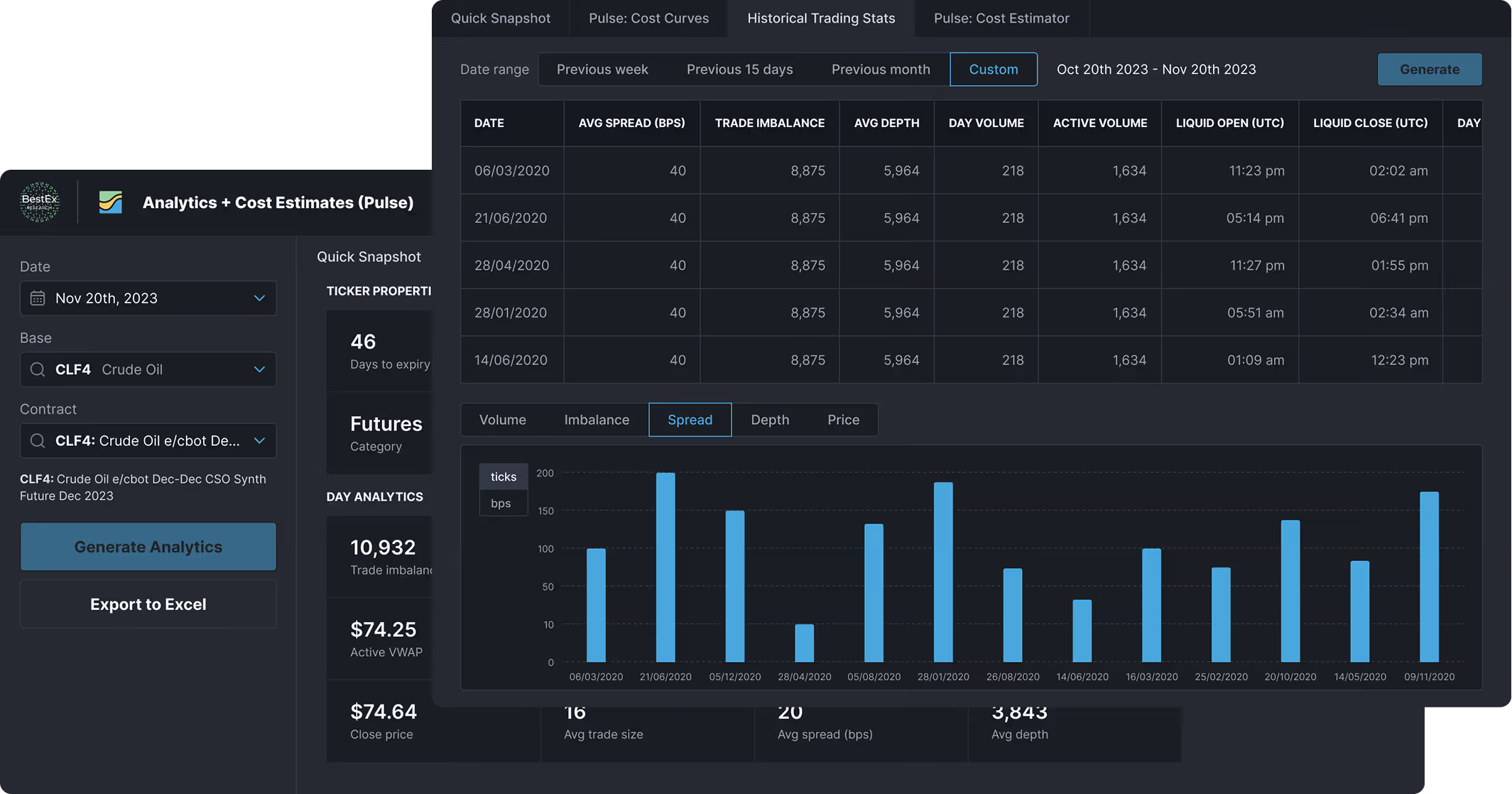

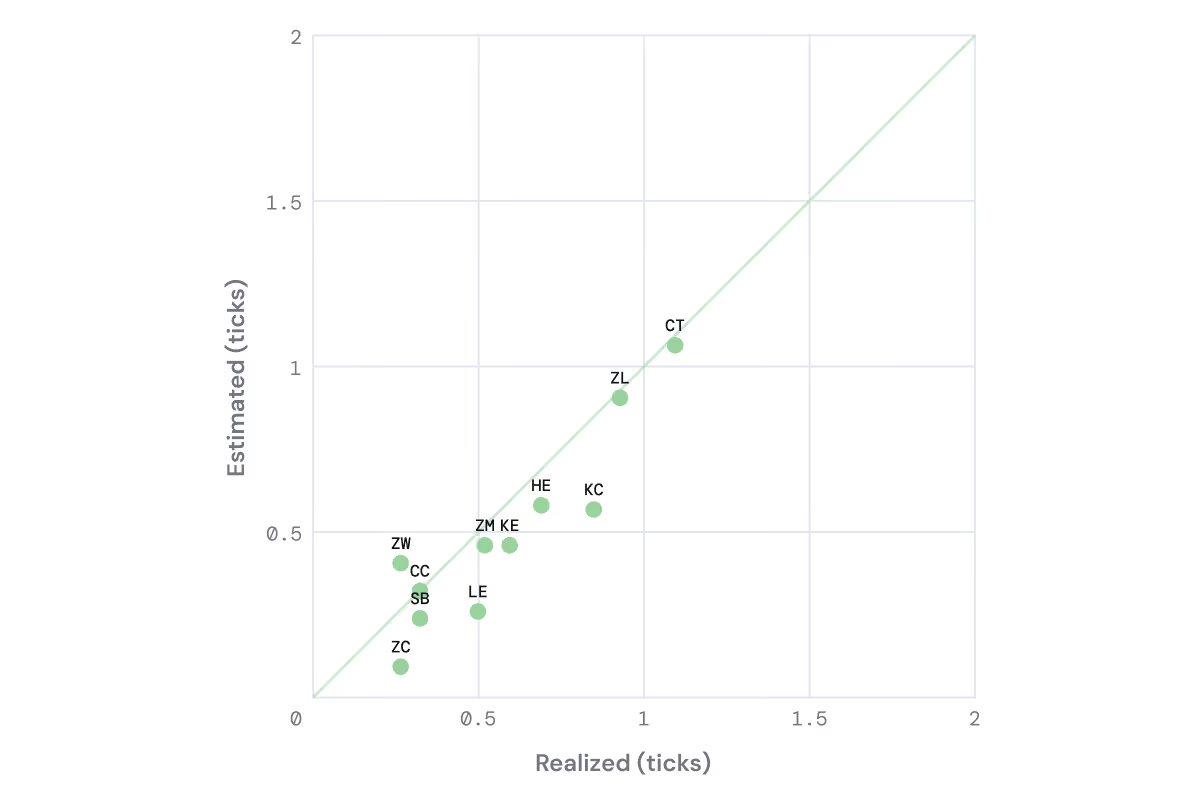

Pulse: A Novel Transaction Cost Model for Futures Trading

Traditional cost models fail to capture the shadow liquidity, large tick sizes, and intraday liquidity variations unique to futures. Pulse offers a unique model for each base symbol and uses a novel normalization method to generate robust estimates of costs, separated into market impact and order placement components.

1 tick

Average difference in realized and projected costs

The chart above illustrates Pulse cost estimates vs. realized cost. Our market impact model’s estimates agree with realized parent order cost data (within a single tick) overall and by product category for more than 72,000 parent orders across product categories (65+ base symbols).

Pulse:Market impact model & pre-trade analytics

Available via REST API & AMS One