AMSOne

The institutional algo platform you would build. Without the investment.

AMSOne is a global, multi-asset algorithmic execution platform with high-performance algorithms, routing, customization, monitoring, analytics, and TCA.

A proven algorithmic execution platform that adapts to your needs

Built by market structure experts, trusted by institutions

Developed by industry pioneers with deep expertise in market microstructure and algorithmic trading. Our platform and algorithms have executed trillions in notional value, delivering proven performance for institutional clients.

End-to-end platform for service at scale

Service hundreds of clients with ease with our Algorithm Management System (AMS). Access a central hub for trade monitoring & control, pre-trade analytics, strategy customization, and transaction cost analysis.

High-performance algorithms

Outperform from day one with our unmatched suite of algorithms backed by empirical research on millions of executions and foundational differentiators proven to enhance performance.

Global, multi-asset coverage

Trade equities and futures across the US, Canada, Europe, and Asia in a unified platform with algorithms customized to each market's unique structure and each product's unique characteristics.

Unprecedented strategy customization

Design completely customized, branded execution strategies with our point-and-click interface. Reduce the timeline for building platform-wide or client-specific algos from days to minutes.

Zero cost of ownership

Deploy institutional-grade execution technology without the traditional eight-figure infrastructure investment. Receive market data feeds, venue connectivity, and ongoing maintenance—all included in your subscription.

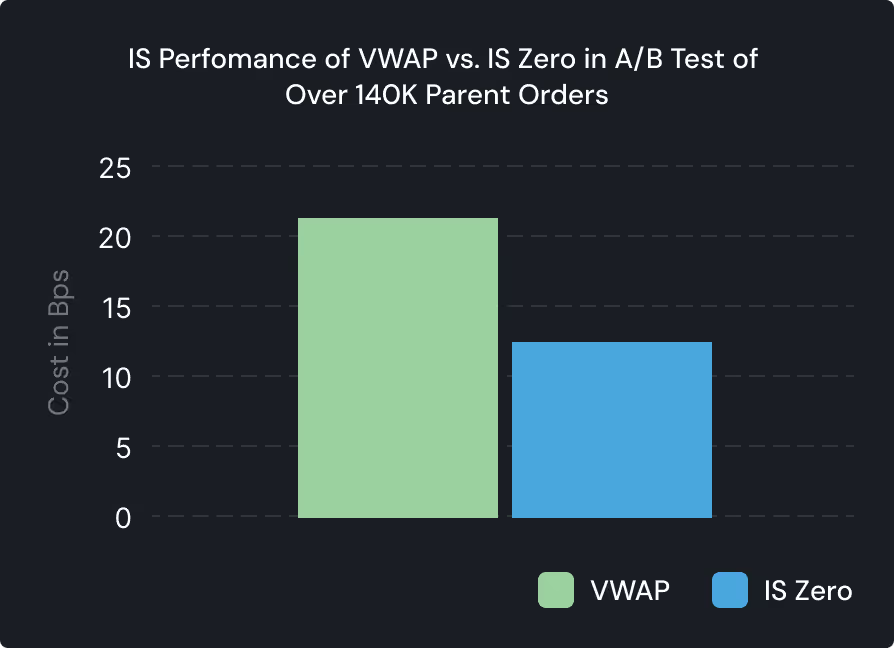

IS Zero: For clients using VWAP algorithm with IS benchmark

BestEx Research’s IS Zero reinvents the VWAP approach by integrating both intraday volatility and volume expectations. IS Zero also pays special attention to illiquid stocks by allowing more flexibility. Over a large sample of tens of thousands of parent orders in an A/B test, IS Zero reduced IS slippage over the VWAP algorithm by 37%.

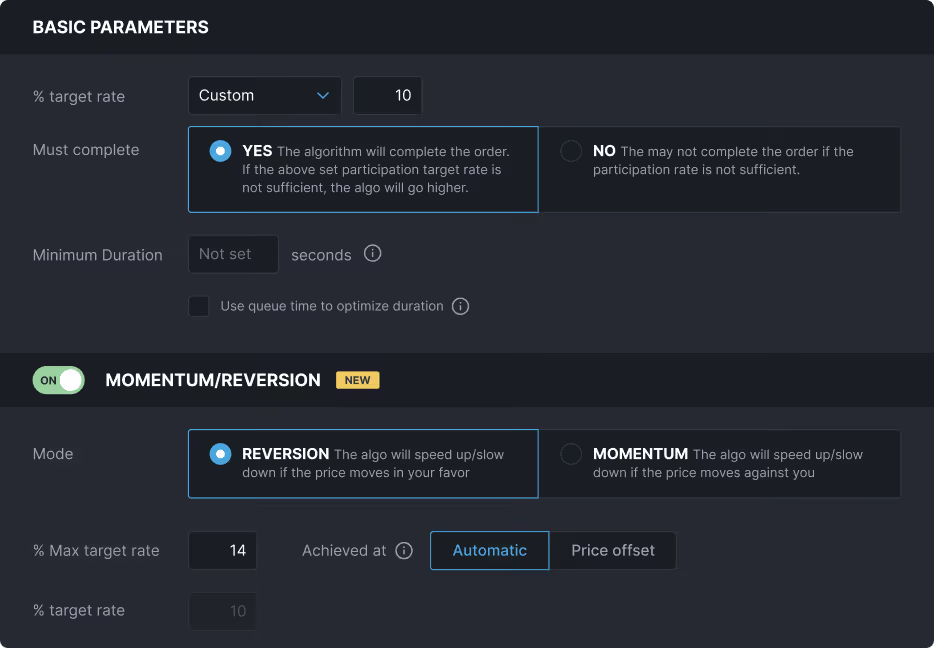

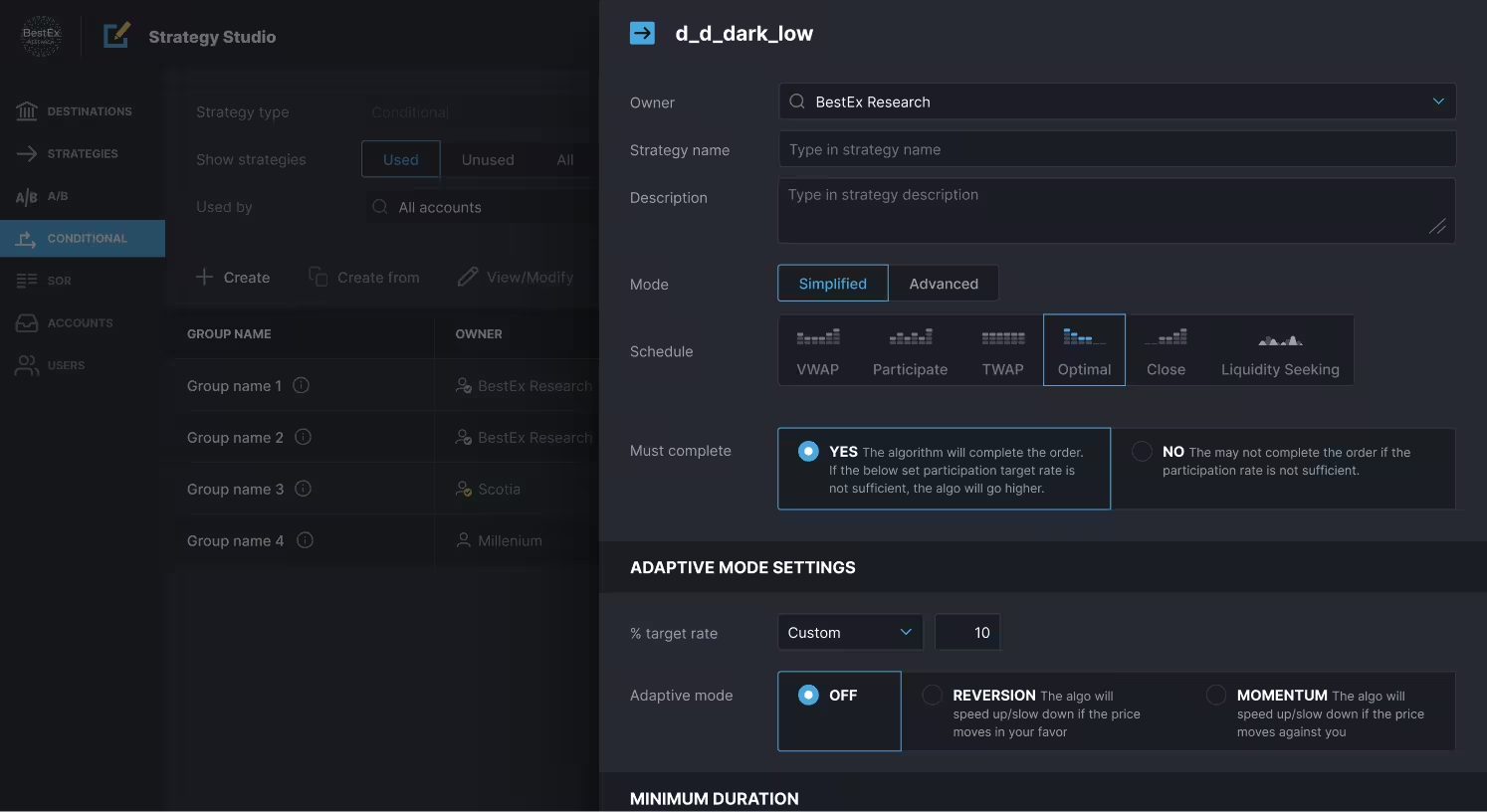

Adaptive Optimal (IS) Framework

Each client segment has unique preferences for urgency and alpha profiles. Some may favor a reversion-based approach, while others lean toward momentum. Some clients prioritize order completion, whereas others focus on minimizing market impact.

Traditional IS algorithms are rigid, offering three urgency levels that do not capture the needs of all traders. Our Adaptive Optimal framework gives you the ability to create an IS algorithm that fits the unique needs of each of your customers. You can choose to make it Must Complete, Not Must Complete, Benchmark Sensitive or not sensitive, mean reverting or momentum based etc.

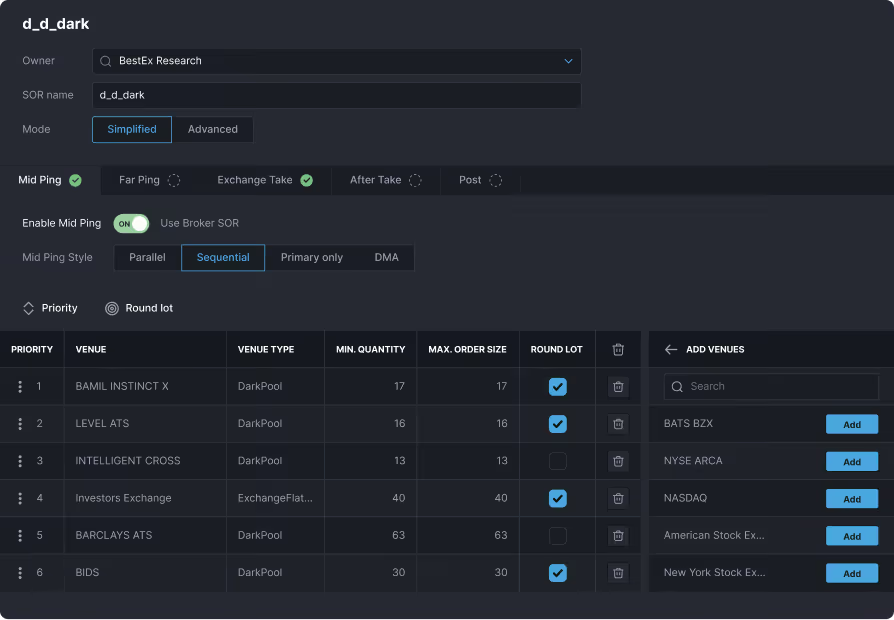

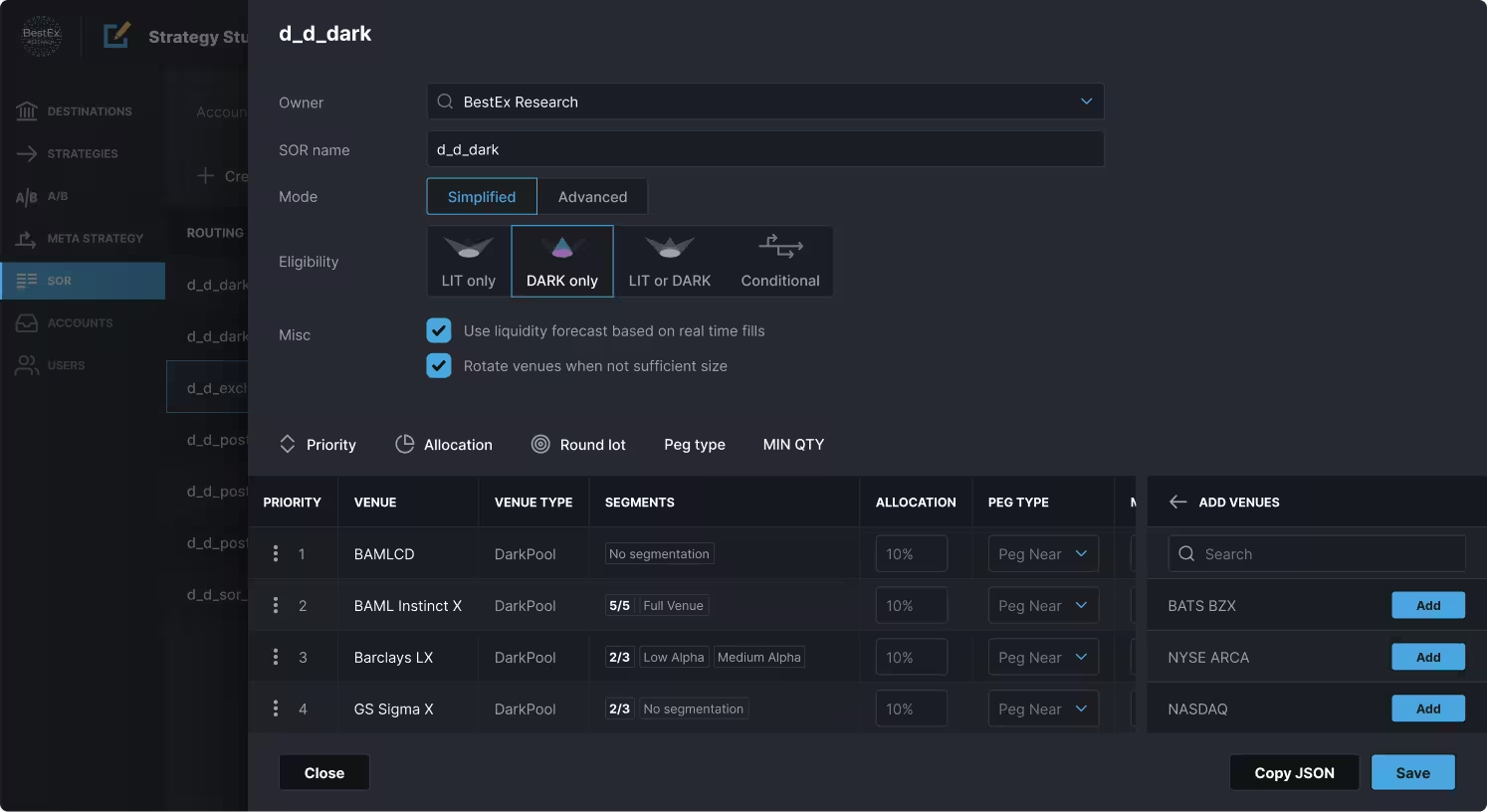

XOR: Design Your Own Lit, Dark & Hybrid SORs

- Sophisticated SORs with several phases

- Each phase can be disabled/customized

- Mid-Ping phase:

- MTFs and exchanges, priority, min size, heatmap, min/max allocation, parallel or serial

- Far-Ping phase:

- MTFs, SIs and exchanges, priority, min size, heatmap, min/max allocation, parallel or serial

- Exchange-Take phase:

- Ability to apply a parallel vs. serial take across MTFs and exchanges

- Post phase:

- Can be Dark or Lit or a combination

Research-driven strategies engineered for performance

IS Zero

Adaptive Optimal

XOR

Curator

TASClose

Smart Conditional

POV

VWAP

TWAP

Close

Built and tested for United States equity market structure

- Execution logic based on US equities market structure expertise paired with empirical research

- Extensive off-exchange venue coverage, accessing more than 97% of dark liquidity

- Robust estimation of critical values impacting trading decisions such as spread, depth, volume, and volatility including a hybrid machine learning methodology that adopts a mix of stock-specific and group-based volume profiles

- Proprietary limit order placement model honors the volume and volatility signature of each stock for maximal spread capture given child order urgency

- Queue-jumping methodology optimizes limit order placement across US equities exchanges

- Curator, a research-driven framework for dark execution, navigates the layered complexity of ATSs including segmentation, tactic selection, signals, minimum quantities, and more to reduce information leakage and adverse selection

Built and tested for Canadian equity market structure

- Our platform is differentiated by its intelligent handling of interlisted stock, accessing liquidity in both US and Canadian markets and returning all fills in Canadian dollars

- For the 260 current interlisted names, a median of 58% of daily liquidity is found in US markets, with 10% of stocks having more than 80% of their liquidity in US markets

- For POV and VWAP algorithms, participation rate and volume cap parameters can be specified for:

- Canadian volume only

- US volume only

- Both US and Canadian volume

- For these stocks, we access all available Canadian liquidity and all dark pools and exchanges in the US

Built and tested for European equity market structure

- Robust order placement tested against months of tick data and European exchange simulator

- Incorporates market data feeds from all MTFs and exchanges in each country for optimal use of Primary vs. EBBO, locked and crossed quotes handling

- Unique auction logic built to handle each exchange/MTF rules and market structure

- Access to most MTFs, SIs, Periodic Auctions, and Conditionals via advanced liquidity-seeking logic

- Advanced liquidity providing and taking logic is built into our fully customizable SOR

- Handling rules such as Large-In-Scale (LIS) waivers, reference price waivers (RPW), and liquidity-based waivers

- Realtime and historical analytics account for each market’s idiosyncrasies, for example: on-exchange vs. off-exchange volume and proper tick size handling

Built and tested for APAC equity market structure

- Execution logic tailored to each specific market structure paired with research and empirical observation

- Market-specific analytical profiles for robust estimation of critical values impacting trading decisions such as spread, depth, volume, and volatility

- Proprietary limit order placement model honors the volume and volatility signature of each stock for maximal spread capture given child order urgency

- Limit order placement incorporates stock-specific queue lengths, layering orders in the limit order book to optimize passive fills; flexibility around schedule is increased as needed to accommodate passive fills on long-queue stocks

Built for the nuances of global market structure

Seamlessly integrated with major EMS/OMS and FCMs, trading 150+ contracts across 21 global exchanges

North America

- CBOE

- CBOT

- COMEX

- CME Group

- ICE US

- MIAX

- NYMEX

- TMX Futures

Europe

- ICE Europe

- Eurex

- ICE Endex

- Euronext Paris

Asia Pacific

- HKEx

- JPS

- SGX

- ASX

Latin America

- B3

Built for the nuances of global market structure

United States

Canada

Europe

APAC

Global Futures

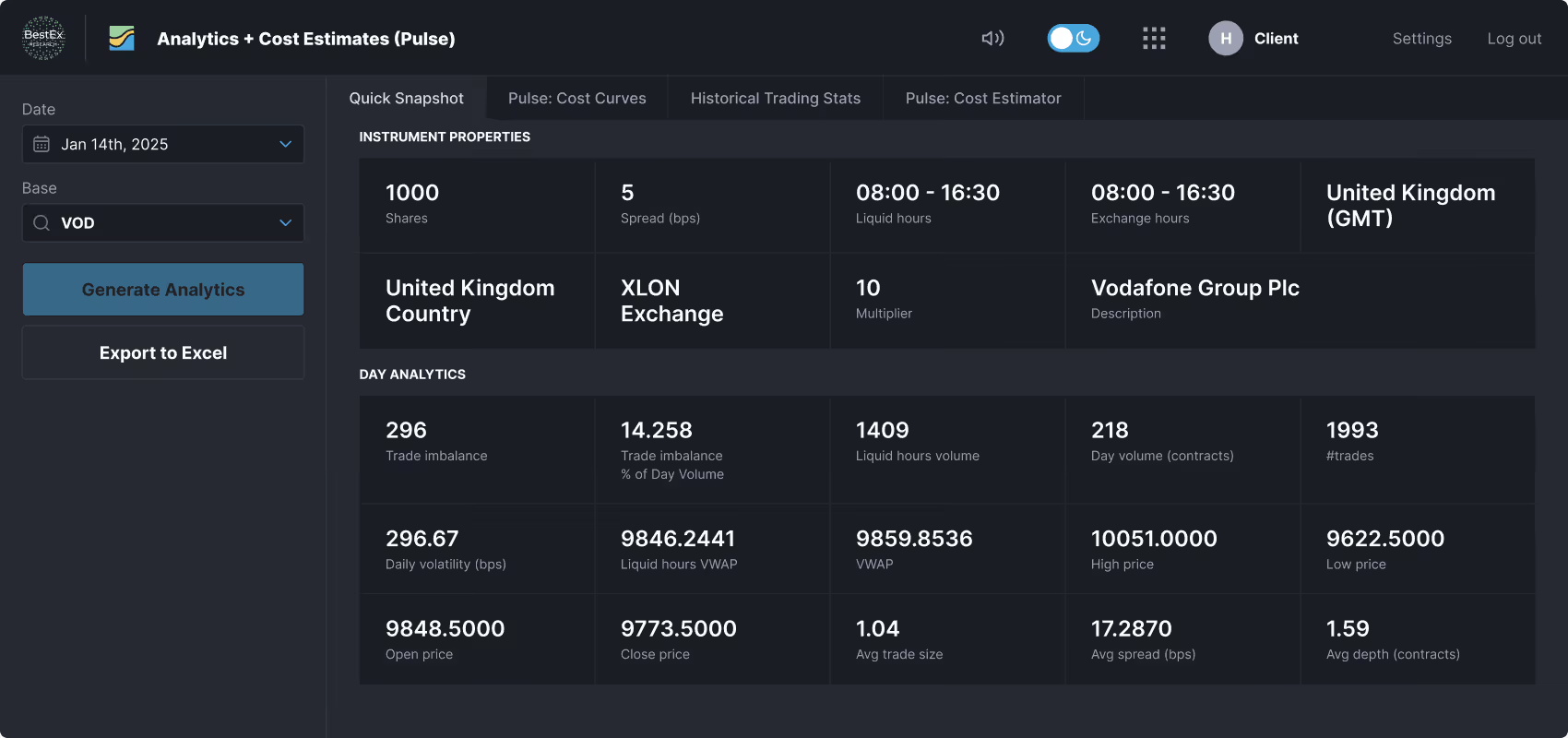

A centralized platform for design, monitoring, & analytics

Real-time transparency and control of algo behavior

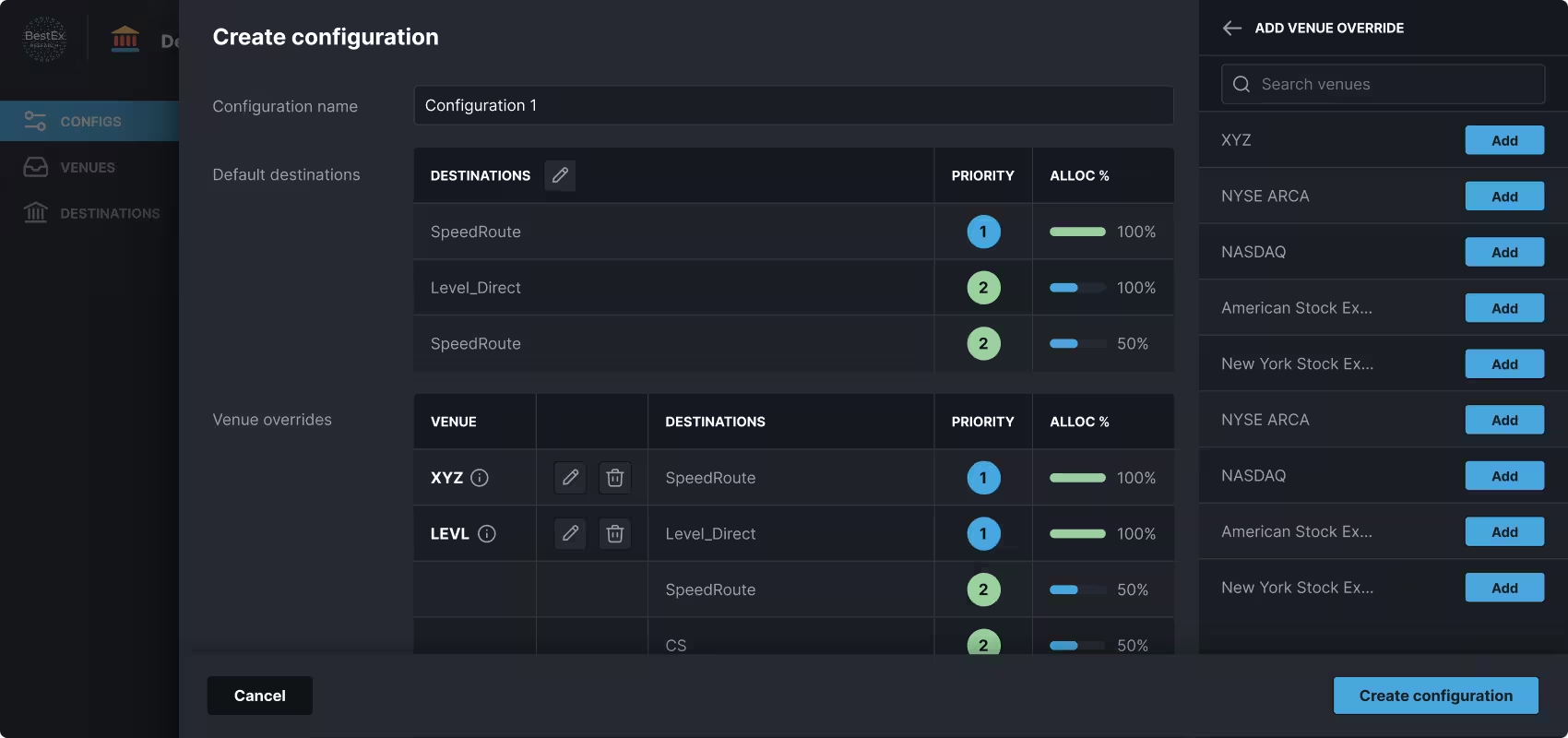

Design custom algorithms and smart order routers

Critical information about your trading, all in one place with our TCA

Estimate market impact and total transaction costs before executing orders

Configure your routes for each venue; specify primary and secondary routes

Dashboard

Monitor child order placement, progress, and performance in real time with complete transparency and control.

- View performance at parent or child order level

- View, modify, pause, and cancel parent and child orders

- Analyze granular metrics: Parameters, Pre-Trade, Progress, Microstrategy, Auctions, Transaction Cost

- Trade alongside algorithms by manually sending child orders

- Filter exhaustively by % ADV, % Volume, % Complete, and more

- Review notifications, audit logs, and risk checks

- Access level 1 & 2 market data

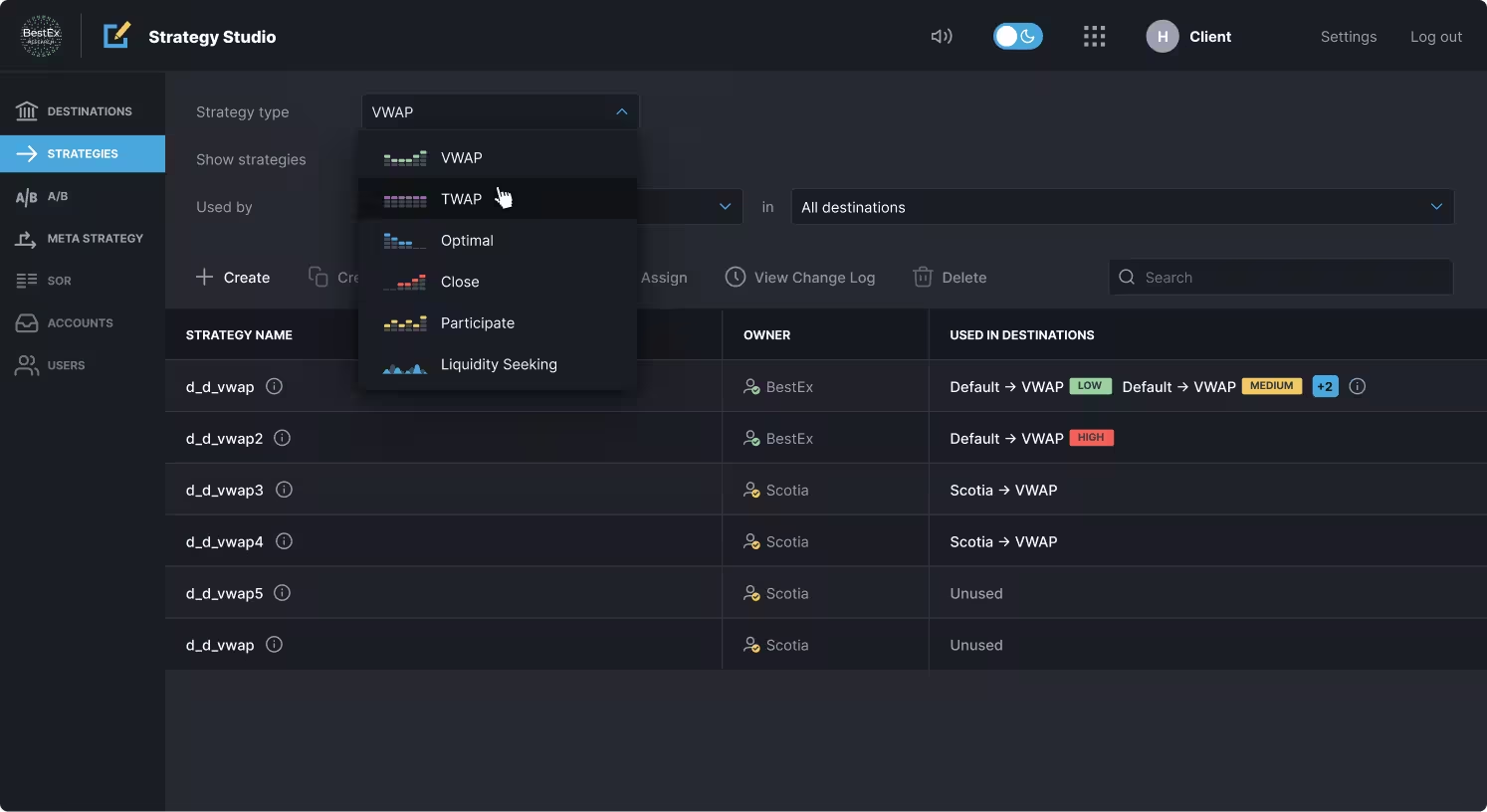

Strategy Studio

Design custom algorithms, SORs, algo wheels, and controlled experiments in clicks without coding.

- Build and modify trading strategies with 150+ unique parameters

- Configure SOR behavior including venue selection, ATS segments, order types, and minimum quantities

- Create dedicated trajectory cross or conditional order SORs

- Set up A/B tests for strategy validation

- Automate strategy selection based on order characteristics

- Available via REST API or AMS One's point-and-click interface

Interactive TCA

- Fully integrated transaction cost analysis (TCA)

- Library of reports for immediate or scheduled delivery

- Evaluate parent and child order performance

- Export data in a variety of formats

- Generate insights for performance improvement and improved strategy design

- Available via REST API or AMS One's point-and-click interface

Pre-Trade

Estimate market impact and total transaction costs before executing orders.

- Model trading costs precisely by time of day and participation rate

- Understand cost components: market impact and VWAP slippage estimates

- Access estimated and realized analytics including spread, depth, volume, and volatility

- Available via REST API or AMS One's point-and-click interface

Routing Rules

Configure your routes for each venue; specify primary and secondary routes.

- Create a wheel of routes with random allocation for each DMA venue

- Create primary / secondary backups

- Implement multiple configurations (e.g., prod vs. beta)

Build and edit strategies in minutes, not months

Fast, easy customization

Every algo change is tested in real time and backtested historically over days or months at high speeds before implementation, the secret to our best-in-industry algo architecture

Over 150 strategy parameters

Parameters related to:

- Scheduling

- Clean up

- Must complete

- Smart Order Routing

- Dark tactics

- Benchmark behavior

- Order placement

- Risk limits

- Auctions

- Order sizing

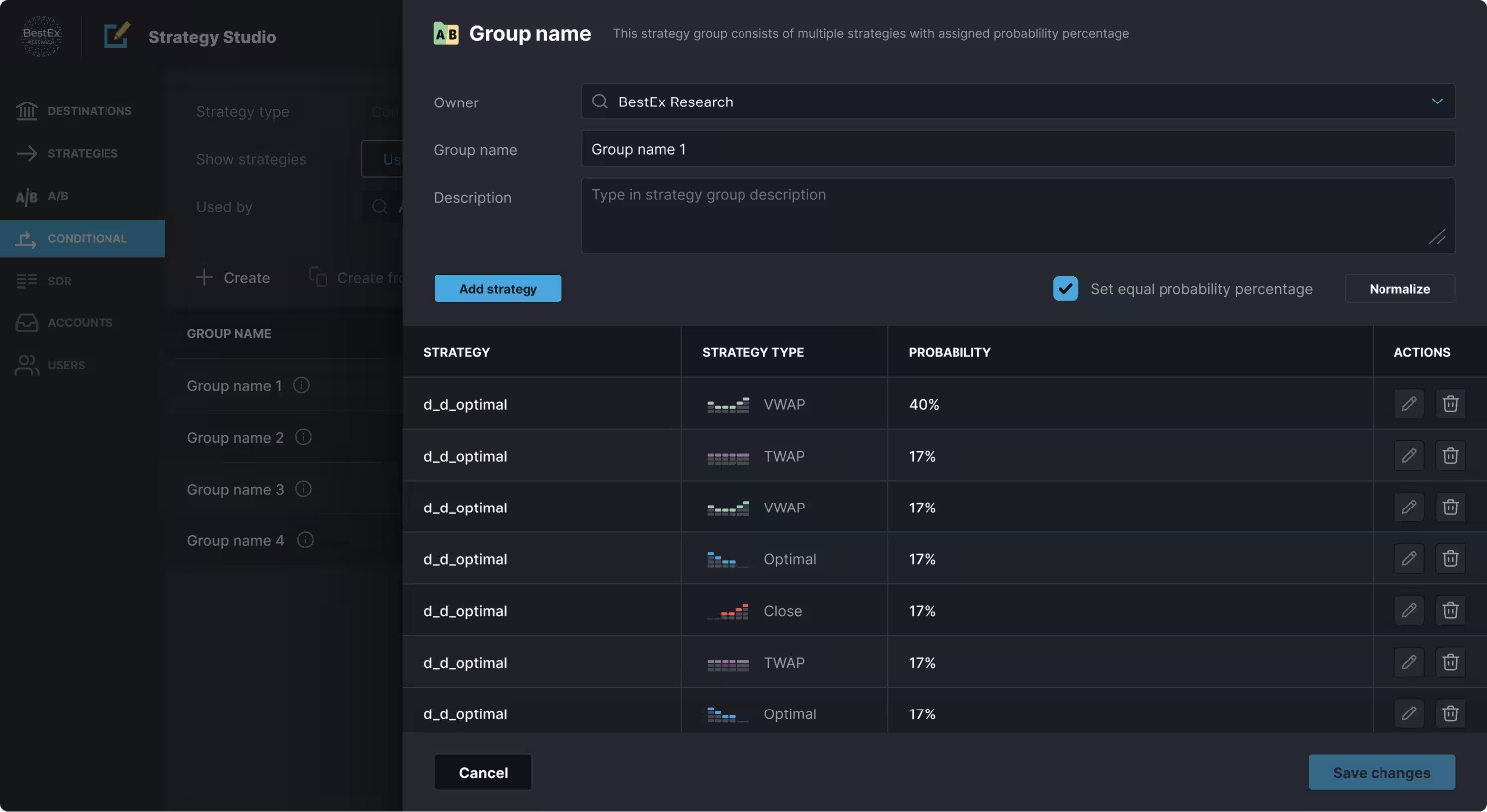

Perform A/B tests across strategies

A/B experiments can be created in just a few clicks in Strategy Studio, randomly routing orders to each strategy as they arrive.

Build custom SORs

- Create custom SORs for lit, dark, hybrid, and conditional market access.

- Add, remove, and prioritize specific venues.

- Customize access conditions such as allocation, peg type, and minimum quantity.

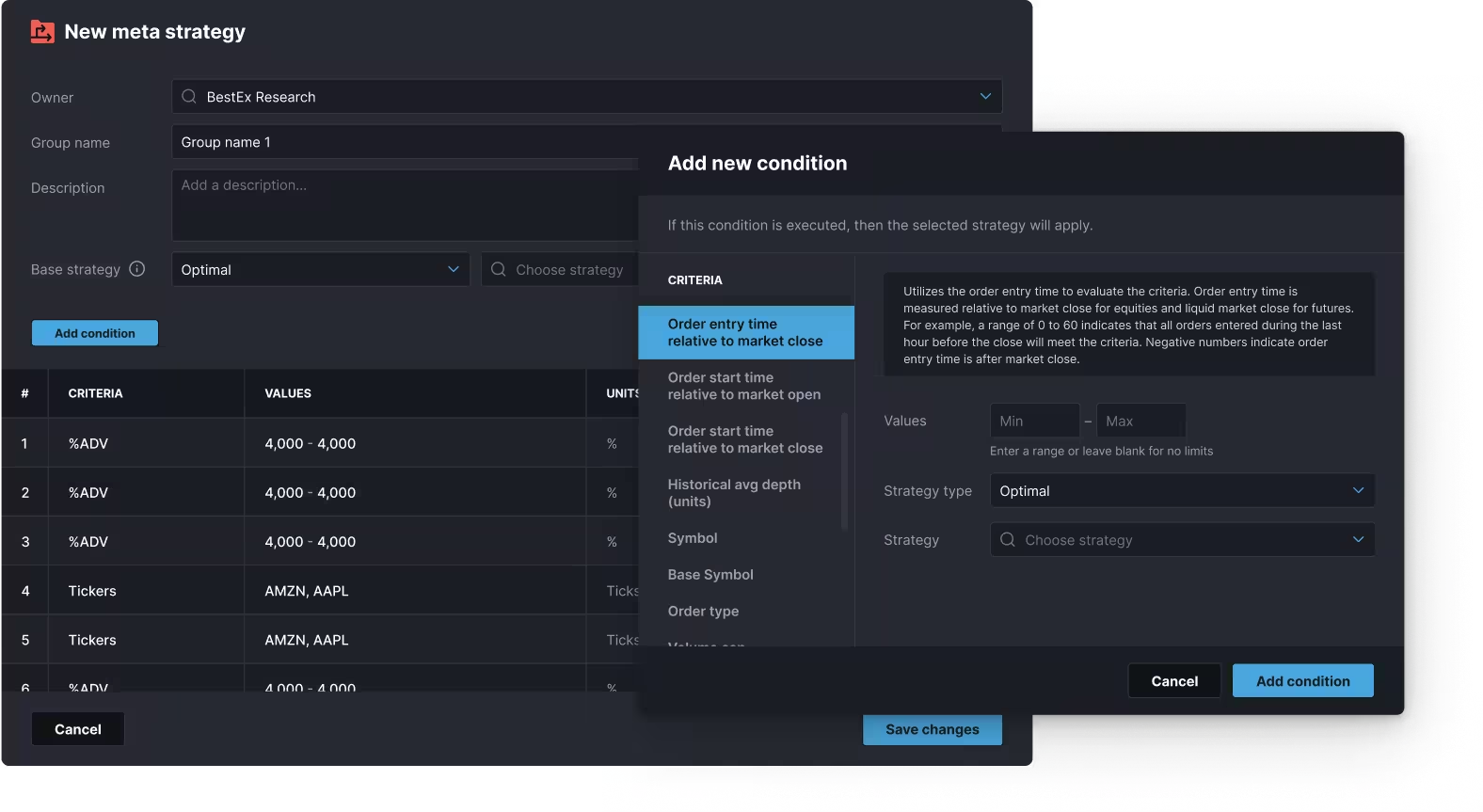

Create Meta Strategies

This feature allows users to create “Strategies of Strategies”, enabling automated strategy selection based on order characteristics:

- Time of day

- Spread

- Country

- Limit vs. market

- Order size

- Expected participation rate

An institutional-grade platform with zero cost of ownership

AMSOne

Build from scratch

Go live only weeks after contract is executed

Takes years for full development from architecture to production

An all-inclusive tiered subscription model to suit your trading volume

Market data feeds, FIX connectivity, co-location, staffing (quants, developers, infrastructure engineers), legal/compliance, and ongoing R&D

Over 150 parameters to customize strategy behavior, overnight. Our service includes complimentary customization support, implemented in days not months.

Requires development time and resources for every modification. Changes are constrained by the complexity of your own codebase and may take months to ship.

The platform scales with your business. We manage load balancing, disaster recovery, strategy testing, and offer dedicated support.

Each new region, asset class, and client account requires additional infrastructure investment and headcount.

Research-driven algo innovation is in our DNA. We keep our technology current with evolving market structure and continuously invest in upgrading AMS and TCA capabilities.

Staying competitive means continuously studying market structure, conducting research, and upgrading systems. This is an ongoing process requiring extensive resources.

Built for performance in every layer

Trading system built in C++

Trading system written entirely in C++ to minimize latency at every stage of order placement, routing, and execution

Realistic exchange simulator

Every algo change is tested in real time and backtested historically over days or months at high speeds before implementation, the secret to our best-in-industry algo architecture

Co-located across the globe

Infrastructure housed in multiple regions for low-latency execution, with full hardware redundancy and automatic failover — delivering 100% system uptime over the past 24 months (as of January 2026)

24x5 monitoring

Our infrastructure supports round the clock trade monitoring and management without system restarts

Always-on execution support

Real-time support via Bloomberg chat, phone, and email

API-ready architecture

Ability to integrate AMS modules with existing systems seamlessly via REST API

Let us walk you through a live demo

Everything your electronic trading business needs, in one platform