.svg)

Optimizing Settlement Execution

Benefiting from Trade at Settlement (TAS) Liquidity & Streamlining Multi-Leg Execution

Trade at Settlement (TAS) contracts are a route to executing at the settlement price of a futures contract without trading the underlying contract itself during the settlement window.

In this article, we analyze liquidity across 29 TAS-eligible contracts over a three-month period and uncover a key takeaway: for many products, the TAS market offers a significant liquidity pool compared to what the settlement window alone can provide.

If you're running a commodity book, managing an ETF, or tracking an index, TAS could have real implications for how you execute. Filling an order in TAS at 0 means you are guaranteed the settlement price. However, your order may not get fully filled at 0, so participating in TAS liquidity has historically required manual coordination of two distinct orders (one in TAS and another in the underlying) which represents substantial operational effort and often creates a tradeoff: give up on TAS liquidity near the settlement window, risk creating impact if your remaining balance is large, or accept the manual overhead.

BestEx Research’s TASClose algorithm handles the optimization problem algorithmically and can increase your access to settlement liquidity while managing the impact in the settlement window, with zero added complexity.

Settlement window liquidity

Settlement prices are typically calculated as a VWAP over a narrow window, often just one to two minutes of trading, depending on the contract. For traders benchmarking to settlement, this creates a structural challenge: execution must occur during a brief period when many participants are targeting the same benchmark. The more volume a trader needs to execute relative to what's available in that window, the more their own activity may push the price away from where the contract was trading at the start of the window, ultimately impacting the benchmark itself.

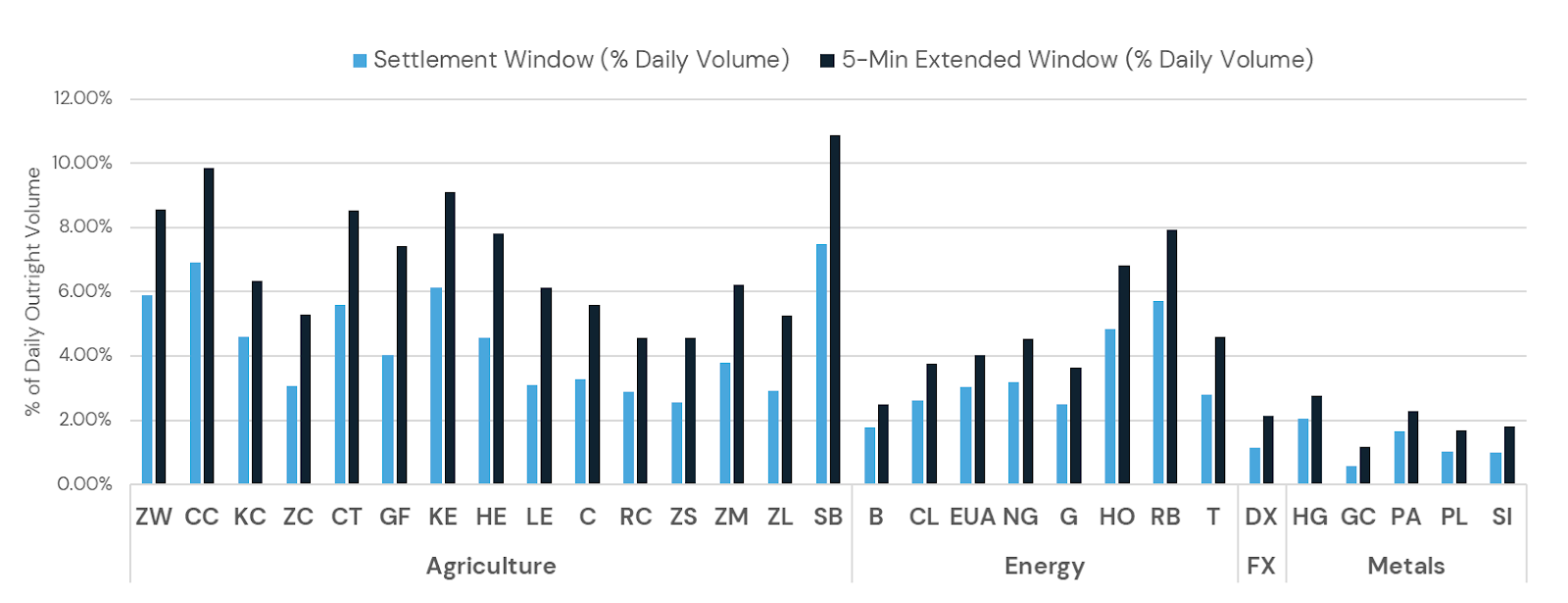

Figure 1 illustrates the settlement liquidity across 29 futures contracts. Our sample (fixed for all results shared in this article) includes the 29 TAS products we trade and their corresponding underlying futures contracts from 12/5/2025 to 3/5/2026. For each, the underlying futures contract is the most active futures contract for each base symbol on each day.

As shown in Figure 1 below, settlement window concentration (shown in blue) ranges from approximately 0.6% of daily volume (Gold, GC) to 7.9% (Sugar, SB). Including the five minutes preceding the settlement window (shown in navy) extends the window’s concentration to between 1.3% and 11.4% of daily volume. Every contract in Figure 1 shows a substantial increase in volume from extending the window, suggesting that a meaningful share of settlement-targeting flow begins accumulating before the formal window opens. For some contracts, volume is doubled (or nearly doubled), including Soy Bean Oil (ZL, an 83% increase), Feeder Cattle (GF, 84%), London Cocoa (C, 85%), Live Cattle (LE, 94%), Soybeans (ZS, 97%), and Gold (GC, 108%).

What is TAS?

Trading at Settlement (TAS) contracts allow traders to lock in a price defined as an offset to the eventual settlement price. TAS contracts are offered for select underlying futures contracts on select exchanges (see our current TAS coverage here).

Pricing of TAS contracts is given relative to the underlying contract’s settlement price; for example, a fill at “TAS 0” equates to the exact settlement price. This means that traders can guarantee fills at a specified price relative to the settlement price without participating in the settlement window itself.

Unlike execution in the settlement window, which is typically compressed into a one or two minute interval, TAS liquidity is accessible throughout the trading session, leading up to and including the settlement window. This gives traders a much wider window to work orders targeting the settlement price.

The magnitude of TAS liquidity

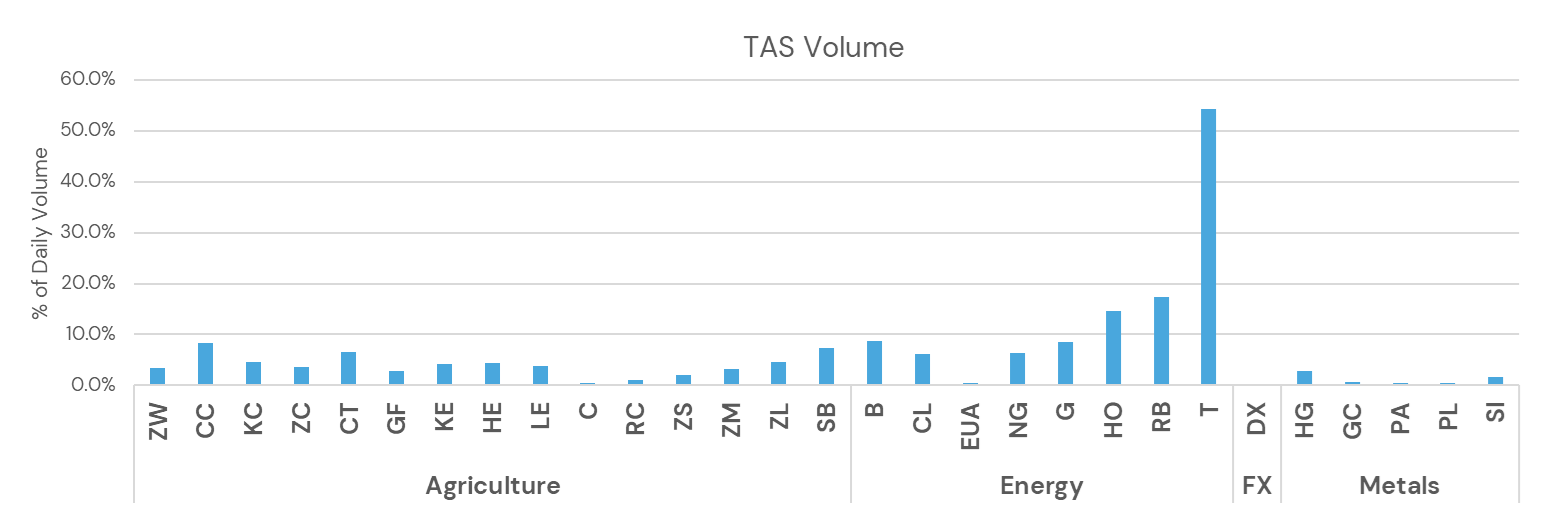

So how much liquidity does TAS actually add? For many products, TAS volume is significant when compared to the underlying contract’s daily volume, as illustrated in Figure 2. Energy TAS products lead the way, with RBOB Gasoline (RB), NY Harbor ULSD (HO), Brent Crude (B), and Low Sulphur Gasoil (G) all exceeding 8% of the underlying’s daily volume. ICE WTI (T) stands out in its TAS volume on average, providing more than 50% the underlying daily volume; however it is important to note that this ratio fluctuates significantly from day to day.

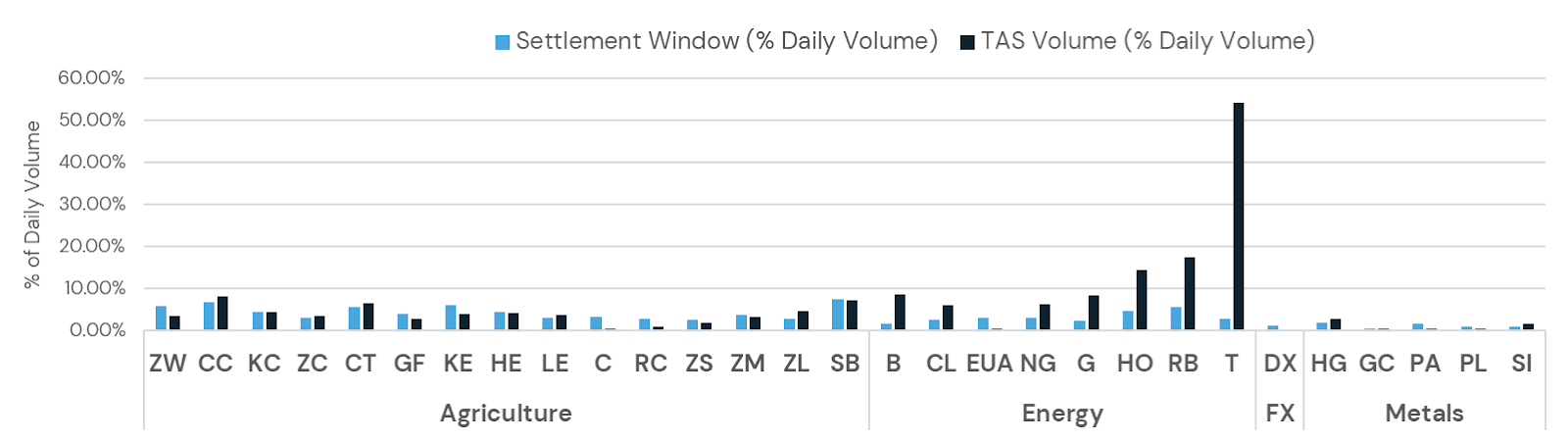

This picture gets clearer when we compare TAS volume versus settlement window volume in the underlying futures contract, side by side. For many contracts, TAS offers an additional 50% of the settlement volume or more as shown in Figure 3. In some cases, TAS volume even exceeds settlement window volume, with the TAS market offering an additional 2, 3, or 4 times larger liquidity pool than the settlement window for the same underlying contract. For many of these contracts, a client seeking the settlement price can access much more liquidity and reduce their market impact by working part or all of the order in the TAS market.

Example: Brent Crude (B) shows TAS volume equivalent to roughly 9% of outright daily volume, compared to approximately 2% traded during the settlement window. On a day with 100,000 lots of outright volume, that translates to roughly 9,000 lots available in TAS versus 2,000 in the settlement window, 4.5 times the volume for a trader targeting settlement price.

The case for using TAS is particularly compelling in energy markets where TAS liquidity is most plentiful. But in most agriculture and metals contracts, TAS also contributes meaningful liquidity, with volumes comparable to those in the settlement window or higher.

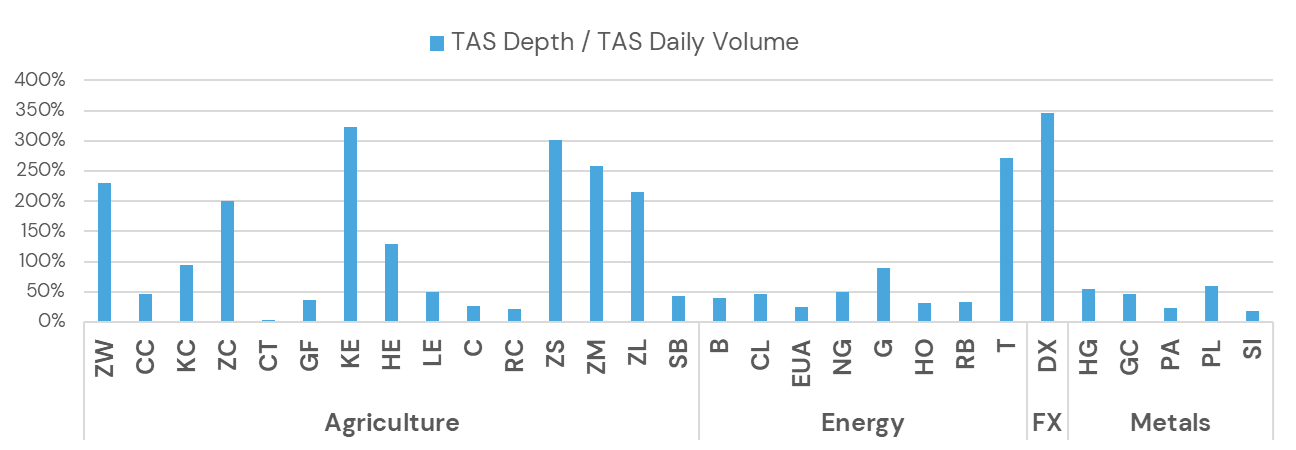

However, achieving settlement price through TAS may not always be an easy trade. TAS markets often have “long queues”, large volumes of child orders waiting passively to trade at the market’s prices. Additionally, the bid and offer depth can be heavily skewed to one side of the limit order book. For this reason, while TAS volume can represent a beneficial source of liquidity, actual TAS execution often requires patience and may result in unfilled child orders. Shown below in Figure 4, TAS market depth exceeds TAS daily market volume in many cases, some by 2-3 times.

Such long queues, as illustrated in Figure 4, can mean zero executions over an algorithmic TAS order intending to trade only at no slippage to settlement price (TAS 0). In this case, there would be no progress made, and the full order quantity would be left to trade into the settlement window. Conversely, when opportunity arises, an algorithm can “pounce”, taking liquidity at 0 when it appears much faster than a human can react. As a result, TAS execution requires consideration and coordination. As we will discuss in detail below, our TASClose algorithm can help optimize TAS execution.

The challenge of multi-leg coordination

While TAS contracts can add liquidity, in practice, using TAS can introduce operational complexity.

Executing against the settlement price (in addition to TAS or alone) involves a series of important strategic decisions. The settlement window is typically just one to two minutes long (sometimes only 30 seconds), and concentrating an entire order within that window can move the price, particularly for larger orders. Traders must consider when to begin executing, how much of the order the settlement window can absorb without meaningful impact, and whether to start working ahead of the window to reduce potential market impact while achieving their objectives. A close algorithm, such as BestEx Research Close, can address these decisions systematically by determining an appropriate start time based on the order's size relative to expected settlement window volume.

When adding TAS to the equation, new questions arise. Traders now have two independent execution paths to manage, one for TAS and one into the settlement window itself, doubling their operational workload. Traders must understand TAS liquidity and determine how exactly to trade in the TAS market (how much? when?), as well as when to give up on TAS and shift toward trading the underlying contract into the settlement window.

Example: Consider working a 1,000-lot Brent order at settlement. There may not be enough liquidity present in the TAS market to fill the order completely at TAS 0, and you don't want to pay up into the order book just to get a fill. Ideally, you would work the order over time at TAS 0 to capture available liquidity at the settlement price, and then route the remainder to the outright market as the settlement window approaches.

This is often achieved via OCO (One-Cancels-Other) order types. However the orders are not co-managed; instead one simply cancels the other at a pre-defined time. This does not dynamically optimize TAS fills and minimize market impact.

Until now, this coordination has been either through a reliable, but static, OCO workflow or a manual, real-time exercise: two separate orders across two execution paths, managed simultaneously under time pressure. Given the operational complexity of manual trading, some traders choose to outsource to a high-touch brokerage desk or skip TAS altogether and pass on the potential benefits.

Streamlining multi-leg coordination with TASClose

The complexity of manual coordination and limitations of existing solutions are the reasons we at BestEx Research created TASClose, an algorithm designed to coordinate TAS and settlement window execution in a single, automated strategy. The algo works TAS at zero or better, taking liquidity up to zero or resting passively at zero to maximize fills at the settlement price. Any residual quantity is automatically routed to our Close algo, which executes the balance before and during the settlement window.

A shared quantity cap keeps both legs of the order synchronized at all times, eliminating overfill risk and the need for manual supervision. The result is access to the full depth of settlement-price liquidity across both TAS and the settlement window, without the operational complexity.

Stop leaving settlement liquidity on the table

If you're currently routing settlement orders to a close algo only or using a high-touch desk for TAS execution, TASClose may help optimize your settlement execution.

We can set up a 20-minute walkthrough to demonstrate how TASClose works and how it fits into your current workflow. Email us at getstarted@bestexresearch.com to schedule a conversation.

TASClose is currently available across 29 TAS-eligible markets including Crude Oil (CL), Natural Gas (NG), Brent Crude (B), RBOB Gasoline (RB), Copper (HG), and Corn (ZC), for both outrights and calendar spreads. We're adding more contracts as our clients request them.